Yield on 30-Year Treasuries Tumbles as Curve Continues to Flatten

Long-term Treasury yields spiraled lower and sparked the biggest two-day narrowing on the yield curve since March 2020.

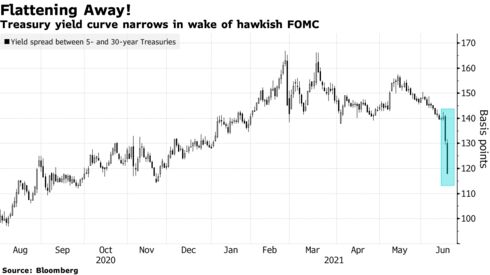

The move came after Federal Reserve officials pulled forward their signal for when monetary policy tightening could start, helping to rein in the risk that inflation might become unmoored.

The 30-year bond yield fell as much as 16 basis points to 2.05% Thursday, its lowest level and biggest intraday drop since February. The plunge in long-end yields comes after new forecasts released Wednesday by central bank officials indicated two rate hikes by the end of 2023, a shift that’s driven up market rates in shorter maturities and put a check on longer-term inflation expectations. The combined flattening since the close on Tuesday was the most since the peak of the liquidity crisis last year.

That dynamic also saw the yield curve, as measured by the gap between 5- and 30-year debt yields, driven to as little as 117 basis points, a level unseen since November.

“Fed credibility as an inflation fighter looks to have green-lighted those worried about buying long duration as an investment to potentially counter-balance other more riskier positions in their portfolios,” said George Goncalves, head of U.S. macro strategy at MUFG Securities Americas.

The sudden flattening of the yield curve also appears to stem from some traders being caught offside after previously positioning for steepening, according to Tom di Galoma, managing director of government trading and strategy at Seaport Global.

Some Wall Street strategists have bailed on prior recommendations to wager on curve steepening.

Following the Fed’s hawkish message at the June policy meeting, reflation trades suffered a “significant setback,” wrote Priya Misra at TD Securities in a note with her colleagues. They recommend exiting 5-year versus 30-year steepeners. Morgan Stanley strategists also exited the same trade, though continue to advocate shorting 10-year breakeven rates.

Money-market traders, meanwhile, have now pulled forward to the final quarter of 2022 their pricing for when the Fed is likely to implement its first quarter-point policy rate increase.

The surprisingly hawkish Fed shift Wednesday induced economists at Barclays to predict that the central bank will formally announce a scaling back of its asset-buying program -- a precursor to actual rate hikes -- at the Fed’s September gathering, with an actual paring of bond purchases to start in November. Barclays had previously predicted a November announcement and a January start date for a change to the bond-buying program, which currently takes in around $120 billion of securities a month.

The net results of the Fed’s actions Wednesday should “be sufficient to tilt the bias of intermediate versus longer-term yield curves toward flattening on better-than-expected data,” Praveen Korapaty, chief rates strategist at Goldman Sachs Group Inc., wrote in note with his colleagues.

Comments

Post a Comment